Greek tourism has proven that it can withstand crises, recover and grow at impressive rates. The question from now on is whether it can truly become sustainable. The answer, as revealed by the PwC study entitled “Is Greek tourism resilient?”, lies in a change of strategy. A strategy that focuses on expanding the product, on the balanced development of Greek destinations, on strengthening cities for short getaways, on reducing dependence on tour operators and on redesigning the country’s winter destinations.

At this point, it should be emphasized that, according to Alexis Chloros, Director, Advisory of PwC Greece, speaking at the Kathimerini Reimagine Tourism 2025 conference, Greek tourism cannot be considered truly sustainable unless it decisively addresses the three threats that act as catalysts for instability:

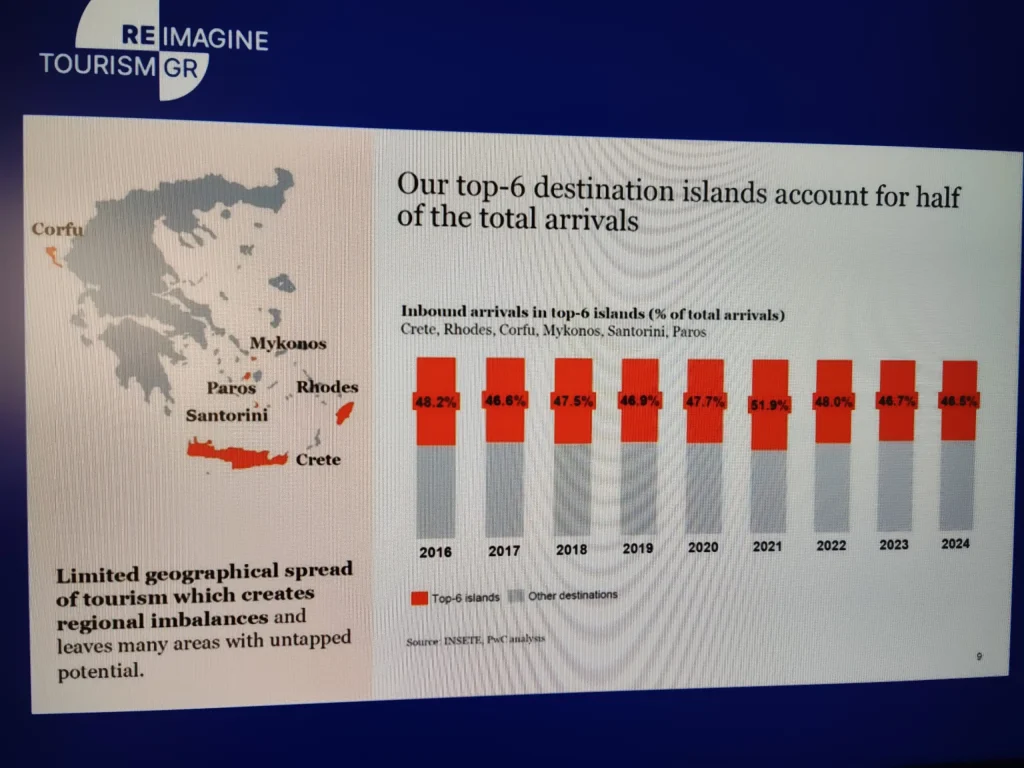

• the overconcentration of flows in a few destinations,

• dependence on a few source countries,

• and seasonality that puts pressure on infrastructure, the environment and the quality of services.

The gap in winter tourism remains chaotic

Meanwhile, winter tourism remains the great unfulfilled bet. Only 5.5% of total visitors choose winter destinations, in a market where flights are few and infrastructure is lagging behind. Areas with authentic wealth, natural beauty and the potential to develop 12-month tourism remain invisible in the international market. This is not just a weakness; it is a missed opportunity that needs to be exploited.

Messinia as a living example of what the country can achieve

In contrast, Messinia is a model of success when tourism is based on planning and infrastructure. With investments, identity, air connections and an international brand, it has seen its arrivals and recognition skyrocket. The model is clear: access, investment, product leads to the development of the entire region, as emphasized.

European practices that show new paths

Gleaning from the European experience, countries such as Finland, the Netherlands, Ireland, Croatia and Cyprus combine sustainability with smart flow management, green routes, slow tourism, agrotourism and revitalization of areas outside the known hotspots. At the same time, cities such as Brussels, Lyon and Dubrovnik are upgrading city breaks, leveraging technology and thematic experiences. In this context, Athens and Thessaloniki can follow the same path, creating a new balance of tourism, as highlighted.

The five main markets determine the course of the sector

In any case, the country remains deeply dependent on five markets – Germany, the United Kingdom, France, Italy, the United States – which generate 43.2% of arrivals and over 53% of revenues. Any disruption in one of these translates into a shock to the system. The financial crisis, the pandemic and Brexit have shown how vulnerable dependence on a few can become.

A model that grows, but relies on a few destinations

The performance of recent years is impressive – 40.7 million arrivals in 2024 and an estimate of 41.5 million in 2025, with revenues of almost 25 billion euros. However, the country’s six top islands – Crete, Rhodes, Corfu, Mykonos, Santorini, Paros – absorb half of the country’s tourism. At the same time, their investment needs have skyrocketed, while other areas with huge potential remain on the sidelines.

The sustainability debate has begun

The presentation of the PwC study at the Kathimerini conference Reimagine Tourism 2025 opens a crucial institutional debate: how Greece will transition from a successful but uneven growth model to a truly sustainable tourism system that will share wealth, protect resources and ensure long-term stability. Greek tourism is indeed on a historically high trajectory. The stakes are no longer to increase the numbers; they are to make the model itself sustainable.

{kind=link}